Good news: Today's 30-year mortgage rates tumble below 6% | March 23, 2023

With rates for all key terms below 6%, borrowers may want to lock in a rate today, ahead of likely increases

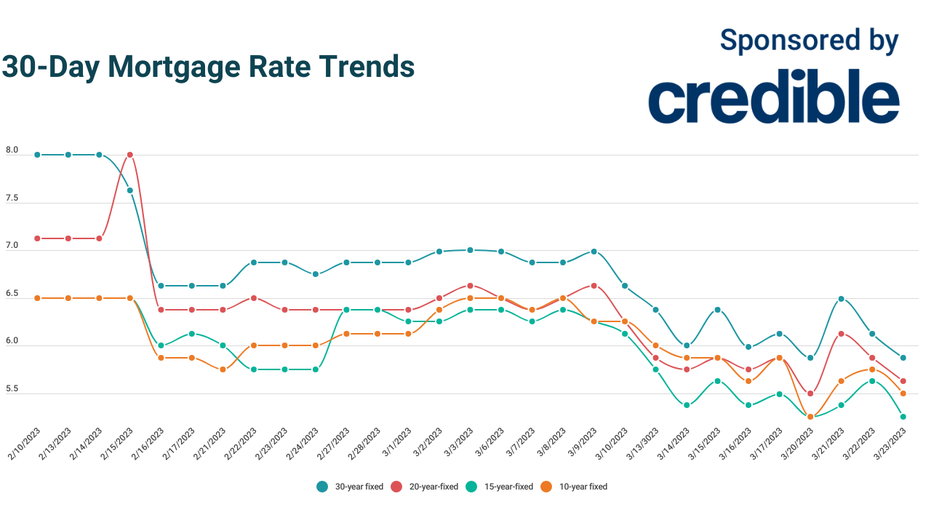

Check out the mortgage rates for March 23, 2023, which are trending down from yesterday. (Credible)

Based on data compiled by Credible, mortgage rates for home purchases have fallen for all key terms since yesterday.

- 30-year fixed mortgage rates: 5.875%, down from 6.125%, -0.250

- 20-year fixed mortgage rates: 5.625%, down from 5.875%, -0.250

- 15-year fixed mortgage rates: 5.250%, down from 5.625%, -0.375

- 10-year fixed mortgage rates: 5.500%, down from 5.750%, -0.250

Rates last updated on March 23, 2023. These rates are based on the assumptions shown here. Actual rates may vary. Credible, a personal finance marketplace, has 5,000 Trustpilot reviews with an average star rating of 4.7 (out of a possible 5.0).

What this means: Mortgage rates have plunged a quarter of a percentage point or more for all key repayment terms today, with 30-year rates diving back below the 6% mark. Homebuyers who want a low interest rate and smaller monthly payments may want to lock in a 30-year rate today, ahead of likely rate fluctuations.

To find great mortgage rates, start by using Credible’s secured website, which can show you current mortgage rates from multiple lenders without affecting your credit score. You can also use Credible’s mortgage calculator to estimate your monthly mortgage payments.

Based on data compiled by Credible, mortgage refinance rates have fallen across all key terms since yesterday.

- 30-year fixed-rate refinance: 5.875%, down from 6.125%, -0.250

- 20-year fixed-rate refinance: 5.625%, down from 5.875%, -0.250

- 15-year fixed-rate refinance: 5.250%, down from 5.375%, -0.125

- 10-year fixed-rate refinance: 5.250%, down from 5.750%, -0.500

Rates last updated on March 23, 2023. These rates are based on the assumptions shown here. Actual rates may vary. With 5,000 reviews, Credible maintains an "excellent" Trustpilot score.

What this means: Mortgage refinance rates have fallen today, bringing rates for all key terms below 6%. Twenty- and 30-year rates dropped by a quarter of a percentage point, while 10-year rates plunged by half of a percentage point. Homeowners who want to stick with a longer repayment term may want to consider 20-year rates, as they’re a quarter of a percentage point lower than 30-year rates. But homeowners who want to take advantage of maximum interest savings may want to consider 10- or 15-year rates, which are the lowest available at 5.25%.

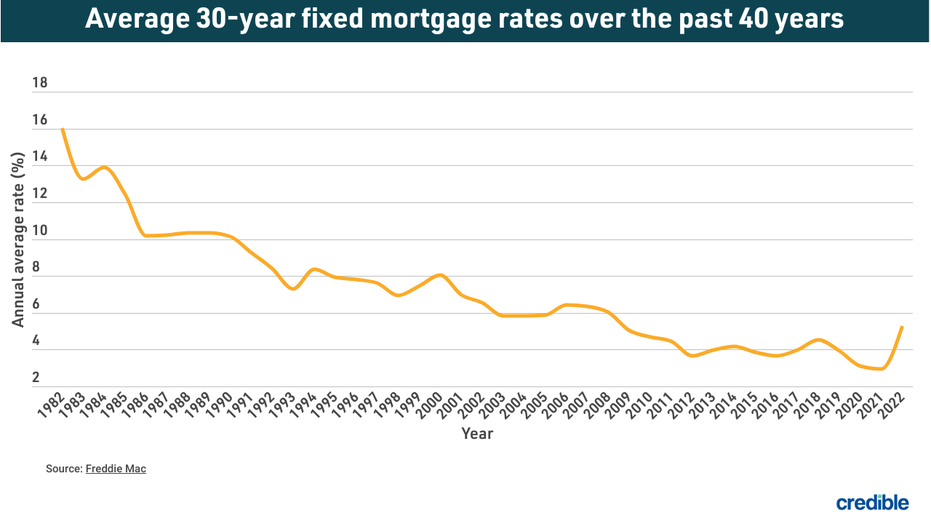

How mortgage rates have changed over time

Today’s mortgage interest rates are well below the highest annual average rate recorded by Freddie Mac — 16.63% in 1981. A year before the COVID-19 pandemic upended economies across the world, the average interest rate for a 30-year fixed-rate mortgage for 2019 was 3.94%. The average rate for 2021 was 2.96%, the lowest annual average in 30 years.

The historic drop in interest rates means homeowners who have mortgages from 2019 and older could potentially realize significant interest savings by refinancing with one of today’s lower interest rates. When considering a mortgage or refinance, it’s important to take into account closing costs such as appraisal, application, origination and attorney’s fees. These factors, in addition to the interest rate and loan amount, all contribute to the cost of a mortgage.

How Credible mortgage rates are calculated

Changing economic conditions, central bank policy decisions, investor sentiment and other factors influence the movement of mortgage rates. Credible average mortgage rates and mortgage refinance rates reported in this article are calculated based on information provided by partner lenders who pay compensation to Credible.

The rates assume a borrower has a 740 credit score and is borrowing a conventional loan for a single-family home that will be their primary residence. The rates also assume no (or very low) discount points and a down payment of 20%.

Credible mortgage rates reported here will only give you an idea of current average rates. The rate you actually receive can vary based on a number of factors.

Getting a mortgage vs. renting

If you’re wondering if you should buy a house or continue renting, no single answer is right for everyone. Whether you should buy or continue renting depends on many factors, including your personal financial situation, long-term goals, preferred lifestyle and market conditions in your area.

Buying a home does come with some distinct advantages that you can’t get from renting, including …

- You can build equity. Home equity can help you build long-term wealth.

- You can personalize your living space more than with a rental that someone else owns.

- Owning a home can provide intangible benefits like pride of ownership, a sense of community and stability.

- Your mortgage payment may be less than rents in your area.

- Mortgage interest is usually tax-deductible.

If you’re trying to find the right mortgage rate, consider using Credible. You can use Credible's free online tool to easily compare multiple lenders and see prequalified rates in just a few minutes.

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.